50/30/20 Budget Rule: Your Simple Guide to Financial Freedom

Master your finances with the 50/30/20 budget rule. Learn how to allocate your income for needs, wants, and savings to achieve financial stability.

Navigating the world of personal finance can often feel overwhelming, with a myriad of budgeting methods and financial advice circulating. However, some principles stand out for their clarity and effectiveness. Among these, the 50/30/20 budget rule has gained significant traction as a straightforward yet powerful framework for managing your money. This guide will demystify the 50/30/20 rule, explaining its components, benefits, and how you can implement it to achieve greater financial control and peace of mind.

Understanding the 50/30/20 Budget Rule Framework

At its core, the 50/30/20 rule is a simple budgeting guideline that suggests dividing your after-tax income into three distinct categories: 50% for Needs, 30% for Wants, and 20% for Savings and Debt Repayment. This approach offers a balanced perspective on spending, ensuring that essential expenses are covered while also allowing for discretionary spending and crucial financial goals.

The beauty of this rule lies in its flexibility and its focus on proportions rather than rigid dollar amounts. It acknowledges that life isn't just about survival; it also involves enjoying experiences and planning for the future. By categorizing your spending, you gain a clearer picture of where your money is going and can make conscious decisions about your financial habits.

Breaking Down the Categories

Let's delve deeper into each of the three categories to understand what they encompass:

The 50% for Needs

This is the foundational pillar of your budget. The 'Needs' category includes all your essential living expenses – the costs required to maintain a basic standard of living. These are the bills and expenditures that, if not paid, would have significant negative consequences on your life. Common examples include:

- Housing: Rent or mortgage payments, property taxes, homeowner's insurance.

- Utilities: Electricity, gas, water, internet, and essential phone services.

- Food: Groceries for home consumption.

- Transportation: Car payments, insurance, fuel, public transport fares, and maintenance.

- Healthcare: Health insurance premiums, co-pays, prescription medications, and essential medical care.

- Minimum Debt Payments: The absolute minimum required payments on loans and credit cards. This is crucial; while extra debt repayment falls into the 20% category, the bare minimum must be covered here.

- Essential Personal Care: Basic toiletries and hygiene products.

It's important to be honest and realistic when defining your needs. While a brand new car might feel like a necessity, its cost might push it into the 'Wants' category if a more affordable, reliable vehicle would suffice. The goal here is to cover the absolute essentials without unnecessary extravagance.

The 30% for Wants

Once your essential needs are accounted for, the next 30% of your income is allocated to 'Wants.' This category is all about discretionary spending – the things that enhance your lifestyle but are not strictly necessary for survival. These are the expenditures that bring joy, comfort, and entertainment into your life. Examples include:

- Dining Out: Restaurants, cafes, and takeout.

- Entertainment: Movies, concerts, streaming services, hobbies, books, and leisure activities.

- Travel and Vacations: Holiday expenses and weekend getaways.

- Clothing and Accessories: Non-essential apparel, designer items, and impulse buys.

- Subscriptions: Gym memberships, streaming services (beyond essential ones), magazines.

- Gadgets and Electronics: The latest technology that isn't strictly required for work or essential communication.

- Home Decor: Non-essential furnishings and decorative items.

This category is where you can truly enjoy the fruits of your labor. The 30% allocation allows for a healthy balance between responsible living and personal enjoyment. It prevents the feeling of deprivation that can often lead to budget burnout.

The 20% for Savings and Debt Repayment

The final 20% is dedicated to securing your financial future and improving your financial standing. This is arguably the most critical component for long-term financial health. It's divided between building savings and aggressively paying down debt.

Savings:

- Emergency Fund: Building a cushion to cover unexpected expenses like job loss, medical emergencies, or major home repairs. Aim for 3-6 months of living expenses.

- Retirement Savings: Contributions to retirement accounts like 401(k)s, IRAs, or other pension plans.

- Long-Term Goals: Saving for significant future purchases such as a down payment on a house, a new car, or further education.

Debt Repayment:

- Extra Debt Payments: Paying more than the minimum on credit cards, student loans, car loans, or any other outstanding debts. Prioritizing high-interest debt can save you significant money over time.

This 20% is your investment in yourself and your future. Prioritizing this portion ensures that you are not just living paycheck to paycheck but are actively working towards financial security, wealth accumulation, and freedom from debt.

Calculating Your 50/30/20 Budget

The first step to implementing the 50/30/20 rule is understanding your net income. This is the amount of money you take home after taxes and other deductions from your paycheck.

Let's use an example. Suppose your monthly after-tax income is $4,000.

- Needs (50%): $4,000 * 0.50 = $2,000

- Wants (30%): $4,000 * 0.30 = $1,200

- Savings & Debt Repayment (20%): $4,000 * 0.20 = $800

Your goal is to ensure that your spending aligns with these calculated amounts. This involves tracking your expenses diligently to see where your money is currently allocated and making adjustments as needed.

Step-by-Step Implementation:

- Determine Your Net Monthly Income: Look at your pay stubs or bank statements to find the total amount deposited after taxes.

- Calculate Your Target Amounts: Multiply your net income by 0.50, 0.30, and 0.20 to get your target spending for Needs, Wants, and Savings/Debt Repayment, respectively.

- Track Your Expenses: For at least one month, meticulously record every dollar you spend. You can use budgeting apps, spreadsheets, or a simple notebook.

- Categorize Your Spending: Go through your tracked expenses and assign each item to either Needs, Wants, or Savings/Debt Repayment.

- Analyze Your Current Allocation: Compare your actual spending in each category to your target amounts. Are you overspending in one area and underspending in another?

- Make Adjustments: If your current spending doesn't align with the 50/30/20 rule, identify areas where you can cut back. This might mean reducing discretionary spending (Wants) or finding ways to lower your essential costs (Needs). Simultaneously, ensure you are allocating the full 20% to savings and debt repayment.

- Automate Savings: Set up automatic transfers from your checking account to your savings and investment accounts shortly after you get paid. This ensures that your savings goals are prioritized.

- Review and Refine: Periodically review your budget (monthly or quarterly) to ensure it still meets your financial goals and adapts to any changes in your income or expenses.

Benefits of the 50/30/20 Budget Rule

Adopting the 50/30/20 rule offers several compelling advantages:

- Simplicity: Its straightforward percentages make it easy to understand and implement, even for those new to budgeting.

- Flexibility: Unlike rigid zero-based budgets, it allows for discretionary spending, making it more sustainable and less restrictive.

- Balance: It promotes a healthy balance between meeting essential needs, enjoying life's pleasures, and securing a financial future.

- Goal-Oriented: The dedicated 20% for savings and debt repayment actively pushes you towards achieving significant financial milestones.

- Reduces Financial Stress: By providing a clear roadmap for your money, it can alleviate anxiety about overspending and financial uncertainty.

- Promotes Financial Literacy: It encourages you to become more aware of your spending habits and make informed financial decisions.

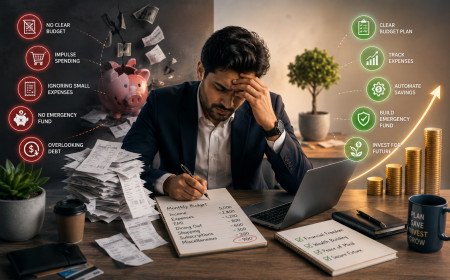

Potential Challenges and How to Overcome Them

While the 50/30/20 rule is highly effective, it's not without its potential challenges. Understanding these can help you navigate them successfully:

- High Cost of Living Areas: In expensive cities, housing and other essential costs might easily exceed 50% of your income.

- Solution: You may need to adjust the percentages temporarily or permanently. Some people opt for a 60/20/20 or even 70/15/15 split if necessary, focusing on aggressive cost-cutting in other areas. Consider lifestyle adjustments like finding a roommate or moving to a more affordable area if possible.

- Significant Debt Burden: If you have substantial high-interest debt, the 20% might feel insufficient to make meaningful progress.

- Solution: Prioritize debt repayment. You might temporarily shift funds from 'Wants' to 'Savings & Debt Repayment' to tackle debt more aggressively. Explore debt consolidation or balance transfer options.

- Irregular Income: For freelancers or those with variable income, applying fixed percentages can be tricky.

- Solution: Base your budget on your lowest expected monthly income. Save any surplus when income is higher. Alternatively, calculate your monthly average income over several months and budget based on that.

- Defining Needs vs. Wants: The line between needs and wants can sometimes be blurry.

- Solution: Be honest with yourself. Ask if the expense is critical for survival and well-being or if it's something that enhances your life but isn't essential. If you're unsure, err on the side of classifying it as a 'Want' until you've comfortably covered your 'Needs' and 'Savings'.

Tips for Success

To maximize the effectiveness of the 50/30/20 rule:

- Be Realistic: Don't set yourself up for failure by creating an unattainable budget.

- Track Consistently: Regular tracking is key to understanding your spending patterns.

- Automate Your Savings: Make saving and investing a non-negotiable habit.

- Review Regularly: Life changes, and so should your budget.

- Seek Professional Advice: If you're struggling, a financial advisor can offer personalized guidance.

- Celebrate Small Wins: Acknowledge your progress to stay motivated.

Conclusion: Your Path to Financial Clarity

The 50/30/20 budget rule offers a balanced, accessible, and effective approach to personal finance. By dedicating specific proportions of your income to needs, wants, and savings/debt repayment, you can gain control over your spending, reduce financial stress, and actively work towards your long-term financial goals. While it requires diligence and occasional adjustments, its simplicity and flexibility make it an ideal framework for anyone looking to build a healthier financial future. Start implementing the 50/30/20 rule today and take a significant step towards achieving financial freedom and peace of mind.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

We focus on content that stays useful over time. Instead of chasing short-lived trends, we create evergreen articles, guides, tips, and educational resources designed to deliver long-term value. Our team works to ensure every article is clear, reliable, and helpful for readers seeking trustworthy information online

Comments (0)