How to Build Long-Term Success Through Financial Planning

Master your future with expert insights into strategic financial planning. Learn how to build lasting wealth, manage risks, and achieve your long-term goals.

Financial success is rarely the result of a single windfall or a lucky investment; it is the byproduct of disciplined, strategic planning that spans decades. Building a legacy requires a shift in perspective, moving away from short-term gains toward a framework that accounts for market volatility, inflation, and changing life circumstances. By establishing a robust financial infrastructure today, individuals can create a foundation that not only sustains their lifestyle but facilitates generational wealth creation.

The Architecture of a Financial Foundation

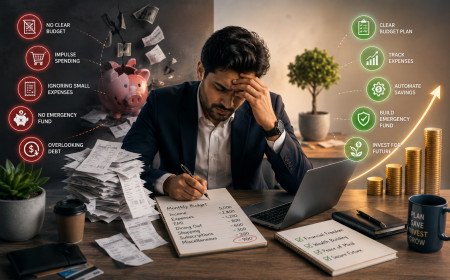

Before any investment strategy can be effective, one must establish a bedrock of financial stability. This begins with an exhaustive audit of current cash flow. True financial planning requires a granular understanding of where capital is allocated. It is not merely about cutting expenses but about optimizing the deployment of resources toward high-yield assets. A professional approach involves categorizing expenditures into essential needs and growth-oriented investments, ensuring that the former is minimized through efficiency while the latter is maximized through consistent contributions.

Emergency liquidity represents the first line of defense in this architecture. Without a buffer of liquid assets—typically covering six to twelve months of living expenses—the entire long-term plan remains vulnerable to external shocks. Market downturns, employment gaps, or unexpected medical costs often force individuals to liquidate long-term investments at inopportune times, effectively destroying the power of compound interest. By maintaining a separate, accessible emergency fund, you insulate your long-term portfolio from the necessity of premature withdrawals.

The Power of Compounding and Time Horizon

At the heart of long-term success lies the mathematical phenomenon of compounding. Time is the most potent asset in any investor’s toolkit, yet it is frequently undervalued. When returns are reinvested, they generate their own earnings, creating an exponential growth curve that is difficult to replicate through active trading or speculative ventures. To leverage this, one must move beyond the noise of daily market fluctuations and adopt a multi-decade outlook.

Strategic asset allocation is the primary vehicle for this growth. Rather than chasing the latest market trends, a successful plan dictates a diversified portfolio tailored to specific risk tolerances and time horizons. This involves a mix of asset classes—equities, fixed income, real estate, and potentially alternative investments—that do not move in perfect correlation. By rebalancing these assets periodically, investors can systematically sell high and buy low, maintaining their target risk profile without emotional interference.

Managing Risk Beyond Market Volatility

Comprehensive financial planning extends far beyond portfolio management; it necessitates a sophisticated approach to risk mitigation. Life is inherently unpredictable, and a successful strategy must account for the transfer of risk. Insurance planning, for example, is not an expense but a strategic tool for capital preservation. Adequate life, disability, and umbrella liability coverage ensure that one catastrophic event does not derail years of accumulation.

Furthermore, tax efficiency is a critical component of net wealth. Over a thirty-year horizon, the difference between tax-efficient and tax-inefficient investment strategies can result in a disparity of hundreds of thousands of dollars. Utilizing tax-advantaged accounts such as 401(k)s, IRAs, and Health Savings Accounts (HSAs) is essential. A professional financial plan integrates these accounts in a way that minimizes the tax drag on returns, allowing more capital to remain invested and compounding over time.

The Role of Debt in Long-Term Strategy

Debt is often viewed as a purely negative construct, but in the context of advanced financial planning, it is merely a tool that must be managed with precision. High-interest, consumer debt is the antithesis of wealth creation and should be eliminated with urgency. However, strategic leverage, such as low-interest mortgages or business credit, can be utilized to acquire assets that appreciate in value or generate cash flow.

The key to managing debt lies in the cost of capital. If the expected return on an investment consistently exceeds the interest rate of the debt used to fund it, leverage can accelerate wealth building. However, this requires a level of discipline that is often absent in retail investors. For most, the focus should remain on debt reduction until a high degree of financial stability is achieved, followed by a conservative approach to leverage that prioritizes cash flow coverage ratios.

Defining Goals and Adapting to Evolution

Financial goals are not static; they evolve as you progress through different stages of life. The priorities of a young professional focusing on career acceleration and aggressive accumulation are vastly different from those of an individual nearing retirement who must prioritize capital preservation and income distribution. A successful financial plan must be a living document, subject to annual reviews and recalibrations.

These reviews should focus on three core areas:

- Portfolio Performance: Measuring progress against benchmarks rather than absolute dollar gains.

- Life Stage Adjustments: Updating estate plans, beneficiary designations, and risk tolerance as family dynamics change.

- Macro-Economic Shifts: Adjusting for changes in tax law, inflation expectations, and interest rate environments that might necessitate a change in asset allocation.

By treating financial planning as a dynamic process rather than a set-it-and-forget-it task, you remain agile in the face of inevitable economic shifts. Success is rarely a straight line; it is a series of adjustments made within a consistent, long-term framework.

The Psychological Dimension of Wealth

Perhaps the most overlooked element of financial success is the psychological aspect. Human behavior is the greatest enemy of long-term planning. Fear-driven selling during market corrections and greed-driven buying during bubbles are the primary reasons retail investors underperform the indices. Building long-term wealth requires the emotional fortitude to adhere to a plan even when the headlines are dire.

Cultivating a mindset of abundance and patience is crucial. This is often achieved through automation. By automating savings, contributions, and debt payments, you remove the necessity for willpower. When the process is automated, the plan continues to execute regardless of your emotional state. This detachment from the daily mechanics of the portfolio is a hallmark of sophisticated investors who view market downturns not as failures, but as opportunities to acquire quality assets at a discount.

Constructing Your Legacy

Ultimately, long-term financial planning is about creating options. It is about reaching a point where your lifestyle is supported by the fruits of your capital, granting you the freedom to pursue work that is meaningful rather than strictly remunerative. This transition requires a shift from the accumulation phase to the distribution phase, a process that is often more complex than the initial growth phase.

During the distribution phase, the focus shifts to withdrawal strategies that prevent portfolio depletion. This involves understanding the sequence of returns risk—the danger that poor market performance in the early years of retirement can disproportionately damage a portfolio’s longevity. By implementing a diversified withdrawal strategy that pulls from different asset classes based on market conditions, you ensure that your capital remains robust throughout your lifetime.

In conclusion, building long-term success is a rigorous, disciplined pursuit that demands more than just saving money. It requires a holistic integration of tax strategy, risk management, disciplined asset allocation, and emotional regulation. By viewing your financial life through a multi-decade lens and committing to a structured approach, you do more than just build wealth; you build a resilient foundation for a life of autonomy and purpose. The path is not easy, but for those who commit to the strategy, the rewards are both sustainable and profound.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

We focus on content that stays useful over time. Instead of chasing short-lived trends, we create evergreen articles, guides, tips, and educational resources designed to deliver long-term value. Our team works to ensure every article is clear, reliable, and helpful for readers seeking trustworthy information online

Comments (0)