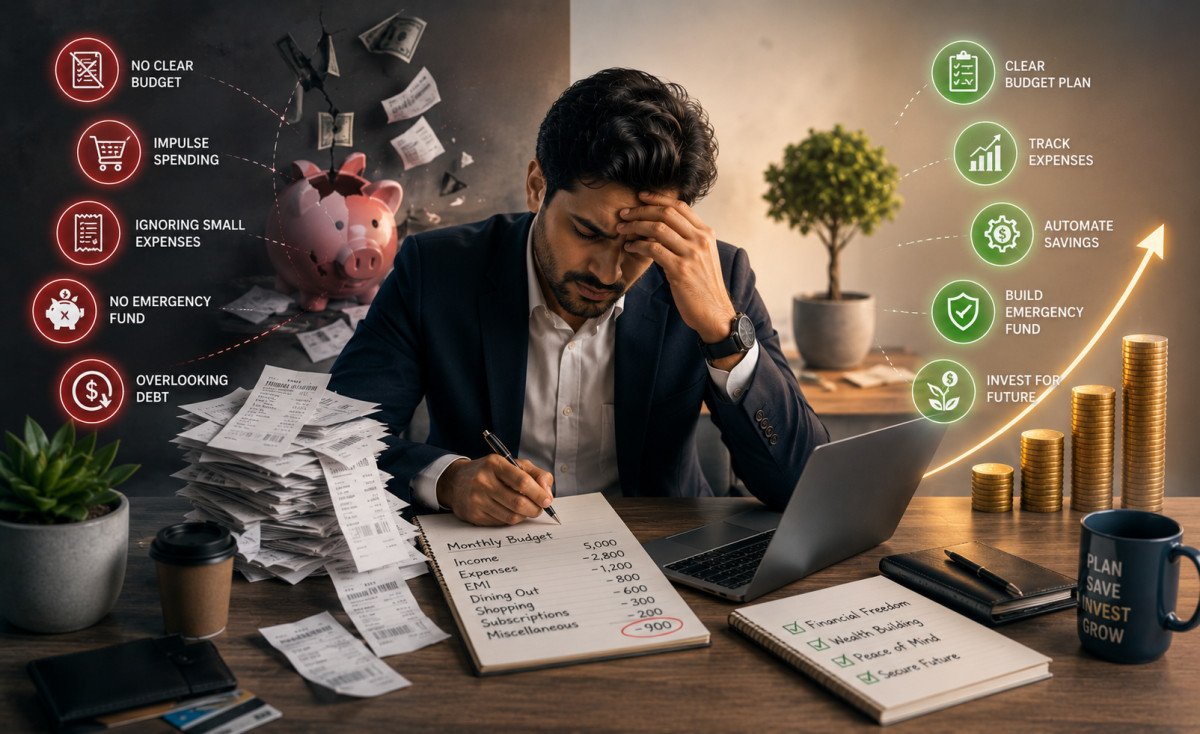

Common Budgeting Mistakes That Ruin Your Financial Goals And How Busy Professionals Can Avoid Them

Discover strategic financial management techniques to avoid common budgeting pitfalls that undermine long-term wealth accumulation for busy professionals.

Managing money can feel like one more task on an already packed schedule. Between work deadlines, family responsibilities, and everyday commitments, it's easy to let budgeting slip down the priority list. Unfortunately, ignoring your finances—even for a short time—can lead to overspending, missed savings opportunities, and long-term financial stress.

The good news is that effective budgeting doesn't require hours of spreadsheets or complicated financial knowledge. Instead, it comes down to avoiding a few common mistakes and building simple habits that support your financial goals.

Whether you're saving for a home, paying off debt, growing your investments, or simply trying to make better use of your income, understanding these budgeting pitfalls can make a significant difference. Let's explore the most common mistakes busy professionals make and the practical strategies that can help you stay financially confident.

Why Budgeting Often Fails for Busy Professionals

Many people think budgeting is only about tracking expenses. In reality, it's about giving every dollar a purpose while staying flexible enough to handle life's changes.

Busy professionals often face challenges such as:

- Irregular monthly expenses

- Limited time to review finances

- Automatic subscriptions and recurring payments

- Lifestyle inflation after salary increases

- Lack of long-term financial planning

When these issues go unchecked, even a good income may not translate into lasting financial security.

Mistake #1: Using the Same Budget Every Month

One of the biggest budgeting mistakes is assuming every month will look exactly the same.

Some expenses remain consistent, like rent or mortgage payments. Others can vary significantly, including:

- Utility bills

- Travel expenses

- Medical costs

- Vehicle maintenance

- Family celebrations

- Seasonal shopping

A fixed budget often falls apart when unexpected costs appear.

A Better Approach: Create a Flexible Budget

Instead of treating your budget as a rigid plan, think of it as a living document.

Start by dividing your expenses into three categories:

Fixed Expenses

These include predictable monthly payments such as:

- Housing

- Insurance

- Loan repayments

- Internet services

Variable Expenses

These change from month to month, including:

- Groceries

- Transportation

- Entertainment

- Dining out

Financial Goals

Reserve money every month for:

- Emergency savings

- Retirement investments

- Debt reduction

- Vacation funds

- Home purchases

Updating your budget monthly takes only a few minutes but can prevent unnecessary financial surprises.

Mistake #2: Forgetting About Automatic Payments

Automatic payments make life easier, but they can quietly become one of the biggest drains on your finances.

Many professionals sign up for:

- Streaming platforms

- Software subscriptions

- Fitness memberships

- Cloud storage services

- Premium mobile apps

Months—or even years—later, they're still paying for services they barely use.

How Subscription Costs Add Up

Imagine paying:

- $12 for one streaming service

- $18 for another

- $10 for cloud storage

- $15 for a fitness app

- $20 for business software

That's over $900 every year without considering other recurring expenses.

A Simple Financial Habit

Schedule a subscription review every three months.

Ask yourself:

- Do I still use this service?

- Does it provide enough value?

- Is there a cheaper alternative?

- Can I pause it for now?

Removing just a few unnecessary subscriptions can free up hundreds of dollars annually.

Mistake #3: Keeping Too Much Cash in a Checking Account

Having money available for everyday expenses is important.

However, leaving large amounts sitting in a regular checking account can slow your financial growth.

Most checking accounts earn little to no interest, meaning inflation gradually reduces the purchasing power of your money.

Build a Three-Level Cash Strategy

Instead of keeping everything in one account, organize your money based on purpose.

Everyday Spending

Maintain enough money to cover:

- Bills

- Groceries

- Transportation

- Monthly expenses

Emergency Fund

Keep three to six months of essential living expenses in a high-yield savings account where your money remains accessible while earning better interest.

Long-Term Investments

Money you won't need for several years may be better placed in diversified investment accounts aligned with your financial goals.

This structure helps balance accessibility, security, and long-term growth.

Mistake #4: Ignoring Small Daily Expenses

Many people carefully plan major purchases but overlook the smaller expenses that quietly accumulate throughout the month.

These include:

- Daily coffee

- Food delivery

- Ride-sharing

- Online impulse purchases

- Convenience store snacks

- Premium shipping fees

Individually, they seem insignificant.

Collectively, they can consume a surprisingly large portion of your monthly income.

The "Convenience Budget" Method

Instead of eliminating these expenses entirely, give them their own budget category.

For example:

- Coffee: $50 per month

- Food delivery: $100 per month

- Ride-sharing: $75 per month

This approach lets you enjoy conveniences without losing control of your overall financial plan.

Mistake #5: Missing Out on Tax-Saving Opportunities

Many busy professionals focus on increasing their income but overlook one of the easiest ways to build wealth—reducing unnecessary taxes.

Tax-saving investment options can help you keep more of your hard-earned money while supporting long-term financial goals. Unfortunately, many people wait until the end of the financial year to think about tax planning, often making rushed decisions.

Make Tax Planning a Year-Round Habit

Instead of scrambling during tax season, review your tax-saving options throughout the year. Depending on where you live, this could include retirement accounts, health savings plans, employer-sponsored benefits, or other tax-efficient investment options.

Here are a few simple habits to follow:

- Review your tax-saving opportunities at least twice a year.

- Take full advantage of employer contributions if they're available.

- Invest consistently instead of waiting until deadlines.

- Keep all financial documents organized for easier tax filing.

Planning ahead not only reduces stress but can also help you save a significant amount over time.

Mistake #6: Spending Doesn't Match Your Financial Goals

One of the biggest reasons budgets fail isn't overspending—it's spending without purpose.

Ask yourself this simple question:

Does the way I spend my money reflect what I truly want to achieve?

Many people say they want to:

- Buy a house

- Become debt-free

- Build an emergency fund

- Retire early

- Travel more

- Start a business

Yet their monthly spending often tells a completely different story.

Without clear financial priorities, it's easy to make impulse purchases that delay bigger goals.

Give Every Dollar a Job

A goal-based budget makes decision-making much easier.

Before making a purchase, ask:

- Will this improve my quality of life?

- Is this worth delaying one of my financial goals?

- Would I rather have this today or achieve my bigger goal sooner?

This simple mindset shift can dramatically improve your saving habits without making you feel restricted.

Mistake #7: Never Reviewing Your Budget

Creating a budget once and forgetting about it is like setting a GPS route but never checking if you've taken a wrong turn.

Life changes constantly.

Your income may increase.

Expenses may rise.

Family responsibilities may grow.

Your financial priorities may shift.

A budget should evolve along with your life.

Schedule a Monthly Money Check-In

You don't need hours to review your finances.

Set aside just 20–30 minutes once a month to answer a few important questions:

- Did I stay within my spending limits?

- Which categories went over budget?

- Have my financial goals changed?

- Am I saving enough each month?

- Are there unnecessary expenses I can remove?

These short reviews help you catch small problems before they become expensive mistakes.

Smart Budgeting Habits That Save Time

Busy professionals don't need complicated financial systems. The best budgets are often the simplest ones because they're easier to maintain.

Here are a few habits that make budgeting much more manageable.

Track Only What Matters

You don't need to record every cup of coffee.

Focus on major spending categories like:

- Housing

- Food

- Transportation

- Savings

- Entertainment

- Shopping

This gives you a clear picture of your finances without becoming overwhelming.

Automate Savings, Not Just Bills

Many people automate their expenses but forget to automate saving.

Treat your savings like a monthly bill.

Set up automatic transfers for:

- Emergency funds

- Retirement savings

- Investment accounts

- Vacation funds

Saving becomes effortless when it happens before you have a chance to spend the money.

Build an Emergency Fund

Unexpected expenses happen to everyone.

Whether it's a medical bill, car repair, or job loss, an emergency fund helps you avoid relying on credit cards or loans.

Aim to save at least three to six months' worth of essential living expenses.

Even starting with a small amount each month can make a big difference over time.

Avoid Lifestyle Inflation

Receiving a salary increase is exciting, but it's also where many budgets begin to fall apart.

As income grows, spending often grows just as quickly.

Instead of upgrading everything immediately, consider using part of every raise to:

- Increase retirement contributions

- Pay off debt faster

- Build investments

- Strengthen your emergency fund

This habit helps your wealth grow alongside your income.

Use Technology Wisely

Budgeting apps can simplify financial management, but don't rely on them blindly.

Technology should help you stay organized—not replace regular financial reviews.

Choose tools that allow you to:

- Track spending automatically

- Monitor savings goals

- Receive bill reminders

- View investment progress

- Generate monthly financial reports

The best budgeting system is the one you'll actually use consistently.

Simple Signs Your Budget Is Working

A successful budget isn't about saying "no" to everything.

Instead, you'll notice positive changes like:

- You know exactly where your money goes each month.

- Unexpected expenses no longer cause panic.

- Savings continue to grow consistently.

- Debt becomes easier to manage.

- Financial decisions feel less stressful.

- You're making steady progress toward your long-term goals.

These small improvements often matter more than following a perfect budget.

Conclusion

Budgeting isn't about restricting your lifestyle—it's about making your money work for you.

The most common budgeting mistakes often have nothing to do with income. They're usually the result of outdated habits, overlooked expenses, or failing to adapt your financial plan as life changes.

By avoiding static budgets, reviewing automatic payments, managing cash wisely, controlling convenience spending, taking advantage of tax-saving opportunities, aligning your spending with your goals, and reviewing your budget regularly, you can build a stronger financial foundation without adding unnecessary complexity to your busy schedule.

Remember, successful budgeting isn't about perfection. It's about consistency. Small, intentional improvements made month after month can lead to significant financial progress over time. Start with one change today, and let each positive habit move you closer to greater financial security and peace of mind.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

We focus on content that stays useful over time. Instead of chasing short-lived trends, we create evergreen articles, guides, tips, and educational resources designed to deliver long-term value. Our team works to ensure every article is clear, reliable, and helpful for readers seeking trustworthy information online

Comments (0)